Recover more from past-due accounts, before they charge off.

Debt Digest is the software lenders use to give past-due customers a fair, self-service way to catch up online, on your brand, on your timeline. You approve every message. Flat per-account subscription: no contingency, no percentage of recovery.

See how the compliance works · built so you stay the only voice your customer hears.

Credit unions today. The broader creditor industry over time.

Two ways your customers catch up · one platform · your brand throughout

Catch up before charge-off

Reach customers while there is still time

Give past-due customers a self-service way to get current before the account is written off, on the timeline your portfolio runs on. Your team approves every notice, and the platform handles the required disclosures and timing. How the timing works.

Settle online, without phone tag

A clear path to a settlement you approve

When a customer or their representative wants to settle, they do it in one online place: offers, counters, e-sign, and payment confirmation, all on the screen. Every offer is checked against the floor you set, so nothing goes below your number.

Firm-negotiated accounts

For post-charge-off accounts with legal representation

When a customer retains a settlement firm, your team works the account through the settlement workspace. Firm submits an offer; your configured floor auto-approves or routes it for review. E-sign and remittance in the same thread.

Live today, and growing as lenders pull us forward.

You decide when members hear from you.

The platform never contacts your members on its own. It prepares each notice for your team, in your name, with the required disclosures and timing built in. Your team presses send. Flat per-account subscription: no contingency, no percentage of recovery.

-

1

Import your accounts

Export from Symitar, CU*BASE, FIS, Jack Henry, or your core. We auto-generate the FDCPA §809(a) validation notice, build a per-account profile, and mark each account as Not Yet Contacted.

-

2

Review who hasn't been contacted

Filter to the Not Yet Contacted queue. See the prepared notice, the channel recommendation, and the TCPA quiet-hours window before anything goes out. Operator-overridable, fully auditable.

-

3

Click to send: you're in control

One button. Notices go out under your credit union's name, your reply-to, your brand. The append-only audit log captures which user clicked, when, and which account moved from pending to sent: examiner-ready by default.

Creditor-initiated

How the three paths actually compare.

Most creditors pick one of three delinquency strategies. Here's what each costs, and what you give up.

| Attribute | Traditional agency | In-house collections | Debt Digest |

|---|---|---|---|

| Pre-charge-off intervention | No | Partial | Yes, 45–115 DPD |

| Typical cure / recovery rate | 10–18% | 15–20% | 25 to 35% cure target |

| Member relationship preserved | Often broken | Varies by agent | Preserved, self-service |

Your legal team wrote our spec, not the reverse.

FDCPA, Reg F, NCUA, FFIEC, TCPA, and state servicer rules are how the platform behaves by default, not what a compliance officer enforces after the fact.

FDCPA §1692eFDCPA §809(a) Validation notice

FDCPA §809(b) Dispute pause

Reg F §1006.6 Outreach windows

Reg F §1006.34 Itemization

NCUA 12 CFR 741.3 120-DPD rule (credit unions)

FFIEC URCC 180/120-DPD rule (banks)

TCPA 47 U.S.C. §227 Quiet hours

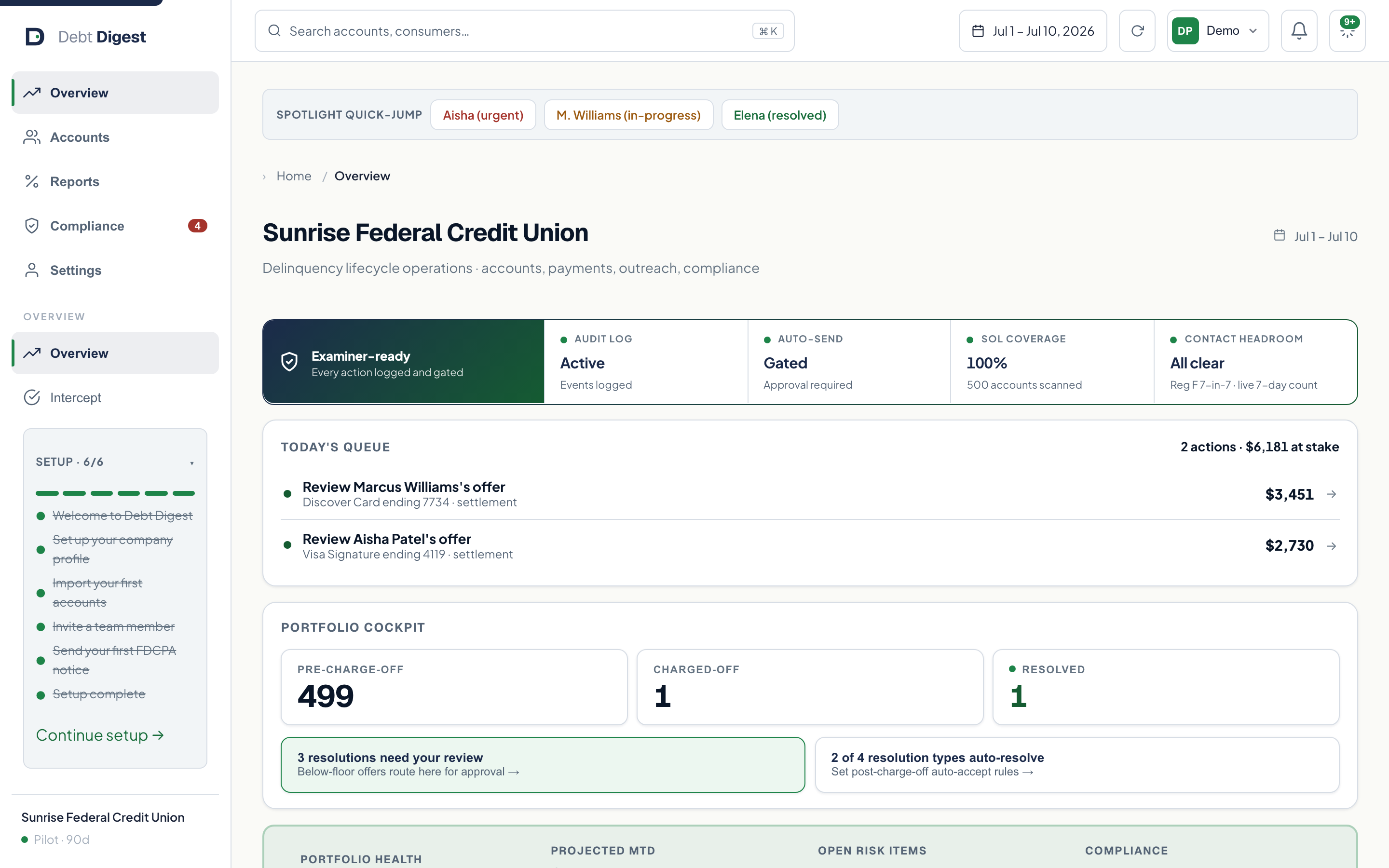

See Debt Digest in action.

The three surfaces your portfolio team will actually use during the pilot.

| Member | Balance | DPD | Status | Outreach |

|---|---|---|---|---|

| J. Martinez | $4,200 | 67 | Delinquent | Plan accepted |

| S. Chen | $12,900 | 104 | 91–115 | Pending |

| M. Williams | $8,400 | 51 | Delinquent | Plan viewed |

| A. Patel | $2,650 | 0 | Cured | 60-day current |

| Member | Balance | Offer | Discount | Status | Days left |

|---|---|---|---|---|---|

| James T. | $4,200 | $2,940 | 30% | Pending | 14 days |

| Sarah M. | $8,900 | $5,340 | 40% | Accepted | n/a |

| David K. | $15,400 | $9,240 | 40% | Declined | n/a |

| Ana P. | $2,800 | $1,960 | 30% | Accepted | n/a |

Ready to see your portfolio here?

Request a pilotSix surfaces. One workspace. Built for the regulator over your shoulder.

Live cures in 30 days. Walk away in 90 if we miss your baseline.

Non-exclusive. Champion-challenger structure. No upfront platform fee. All accounts returned to you on exit, with no lock-in.

Binding pilot agreement. Covers your baseline, pricing, and the 90-day exit clause. Your counsel reviews in one session.

One CSV from Symitar, CU*BASE, or your core. We create member records, generate FDCPA §809(a) notices, and seed outreach profiles per account.

Members self-resolve in the portal. Weekly status reports. Cure rate vs your baseline updates live in your dashboard.

The evaluation is free until you place 100 accounts or 30 days pass, whichever comes first, and does not convert automatically. Continued paid access begins only after a separately accepted subscription order form. Standard pricing is $2.50 per active account per month with a $1,500 monthly floor; there is no per-resolution, outcome, contingency, or percentage-of-recovery fee.

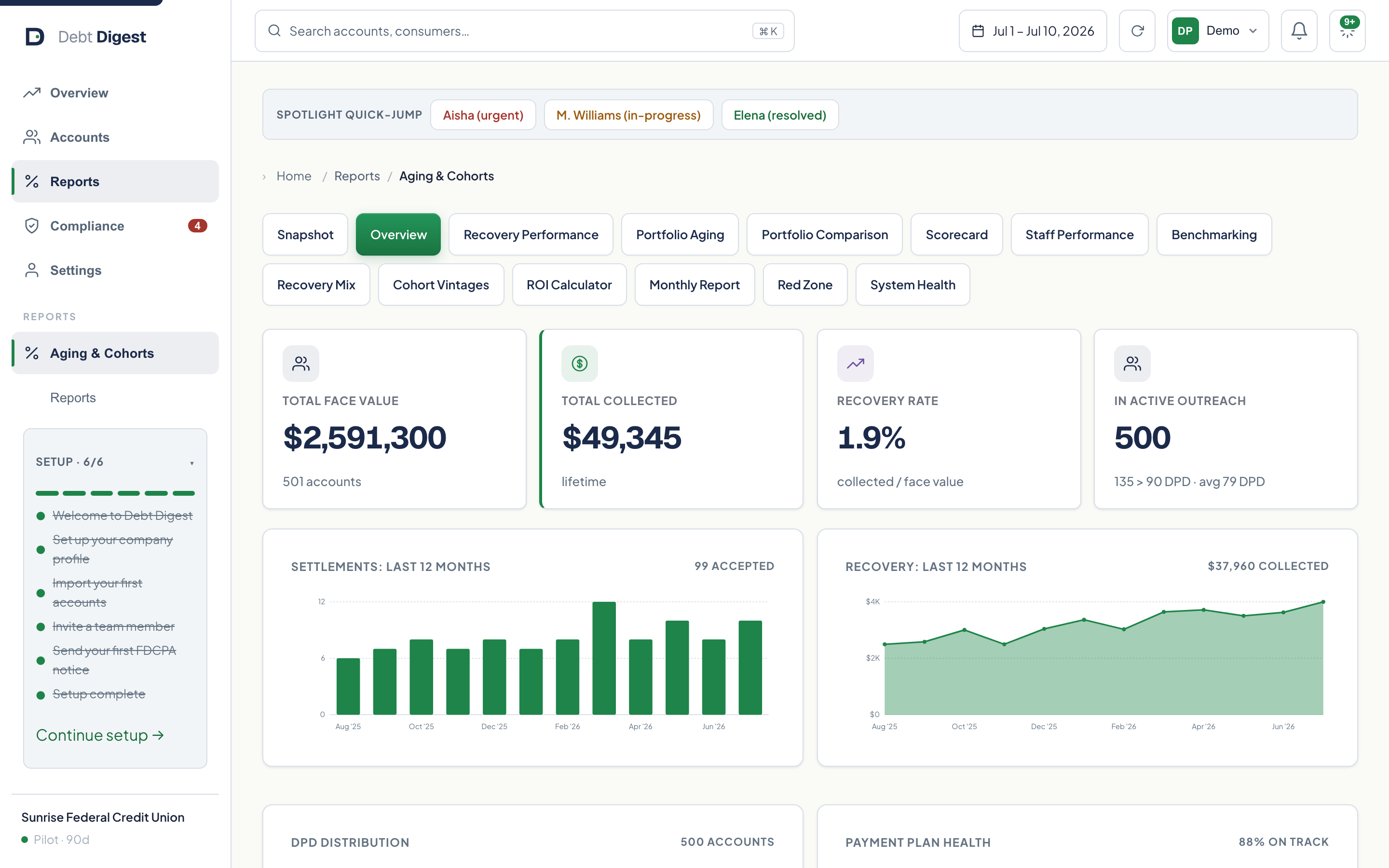

At what cure rate does Debt Digest pay for itself? Almost any.

Four numbers from your last 12 months. See how the platform subscription compares against the incremental recovery your team (or a 25–40% contingency agency) would have left on the table anyway.

Industry default baseline is 10–12%. We report your recovery lift against your own baseline; it is an ROI-reporting benchmark, never a fee trigger. Cure definition: 0 DPD + 60 days current.

Illustrative. The evaluation is $0 until 100 accounts or 30 days, whichever comes first, and does not convert automatically. A separately accepted standard order form is $2.50 per active account per month with a $1,500 monthly floor. No per-resolution or percentage-of-recovery fee.

Subscription pricing that scales with your portfolio, not your recovery.

No per-seat fees. No setup charges. No percentage of recovery. Flat per-account subscription billed monthly.

- Guided onboarding on your brand

- Recovery lift reported against your own baseline

- CSV placement, FDCPA notices, member portal

- Real-time dashboard + audit export

- Founder-led weekly review

- Everything in Pilot

- Outreach intelligence + operator override

- Post-charge-off recovery available

- Online settlements with outside firms

- API access + webhooks

- Everything in Standard

- White-label member-facing portal

- FIS / SS&C / Jack Henry core integration

- Dedicated compliance + success operator

- State expansion handled by DD

Cure definition: account returns to 0 DPD and remains current 60+ days. This is how your recovery ROI is reported, not a billing trigger. Your baseline (your own 12-month history or a 10% industry default) is a reporting benchmark, never a fee basis. Payment flow: member pays you directly. You pay Debt Digest a flat monthly subscription. No percentage of recovery. Detailed terms on /pricing.

Plain answers to the four questions every procurement deck includes.

No spin. If a question doesn't have a clean answer yet, we say so.

Built by someone who has been in the courtroom.

Debt Digest's founder works at a debt-settlement law firm representing people being sued for credit-card debt. Every day, hundreds of clients walk in scared, confused, and convinced they are the only one who is behind. Almost all of them want to pay. They just do not know how, and every collections call they have had made it worse.

The usual model is built around post-charge-off agencies who get paid to pressure. Debt Digest moves the moment of help earlier, takes the pressure out of it, and gives members a path they can actually take, while you stay the only voice they hear.

This is not a collections company trying to sound nice. It is the product we wish existed for every client we have represented.

See the math on your portfolio in 30 minutes.

Send us the size of your 45 to 115 DPD population. We'll model your cure-rate lift, pilot economics, and 90-day rollout plan at no cost, no obligation.

Your accounts. Your settlement floor. Your member relationship.

We're the rails. You stay the holder of the debt, the brand on the screen, and the destination of every dollar.